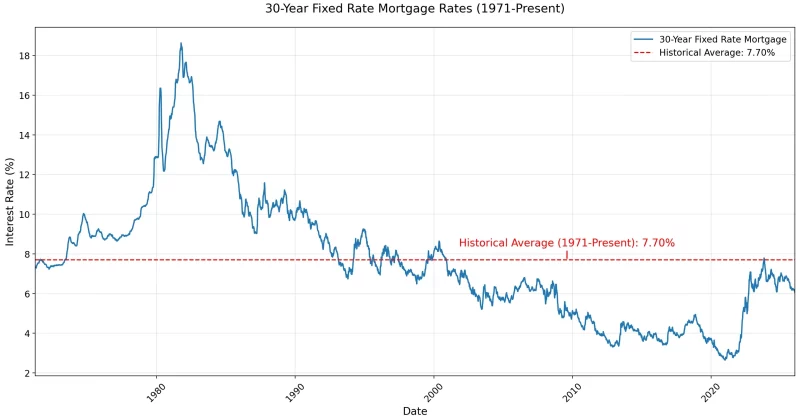

The average 30-year fixed mortgage rate hit 6.51% for the week ending May 21, 2026, according to Freddie Mac. That’s the highest reading since August 2025, and a painful reversal for homebuyers who were enjoying sub-6% rates just a few months ago.

Rising oil prices and persistent inflation concerns are doing the heavy lifting here. What looked like a sustained move toward more affordable borrowing costs has turned into yet another false dawn for the US housing market.

How we got here, and what the numbers say

The climb from sub-6% to 6.51% has been driven largely by geopolitical tensions pushing oil prices higher. Higher energy costs feed directly into inflation expectations, which in turn push up the yields on long-term bonds that mortgage rates track.

For context, the current rate is still below last year’s peaks of around 6.86%.

On a $400K home with 20% down, the difference between a 5.9% rate and a 6.51% rate translates to roughly $120 more per month. Over 30 years, that adds up to more than $43K in additional interest payments.

The crypto-mortgage crossover nobody expected

In March 2026, Fannie Mae approved Bitcoin and USDC as collateral for crypto-backed mortgages. Homebuyers can now pledge their crypto holdings to secure a home loan without selling those assets and triggering a taxable event.

Partnerships between Fannie Mae and crypto platforms like Coinbase are making these products available to a broader audience.

US Treasury research from late 2024 indicated that crypto gains correlate with higher mortgage uptake in low-income areas with substantial crypto exposure. Delinquency rates in these cohorts were reported as low.

What this means for investors

The immediate impact of rising mortgage rates is straightforward: cooling demand. Higher borrowing costs reduce the pool of qualified buyers, which puts downward pressure on home prices and transaction volumes.

For crypto investors specifically, the growth of crypto-backed mortgage products creates real-world utility for holding digital assets. If these products scale, they add a new source of demand for Bitcoin and stablecoins like USDC that goes beyond speculation.

Fannie Mae’s willingness to accept crypto collateral is a significant policy signal, but any tightening of rules around crypto-backed lending could stall the momentum these products are building.